Predicting the Fed

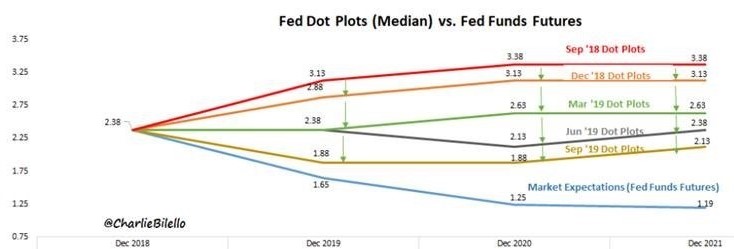

The Federal Reserve concluded a two-day meeting on January 29, announcing no changes to their benchmark rate and releasing their updated “dot plot.” The dot plot illustrates their expectation of the fed funds rate at various times in the future, giving investors some indication of what future monetary policy might be. An upward trajectory signifies a “tightening” cycle of rising rates, while a downward slope indicates an “easing” cycle of declining rates. In the chart below, the red line represents the Fed’s expectations as of September 2018. At that time, they were projecting the fed funds rate to be 3.13% by the end of 2019. Fast-forward to December 2018 (orange line), and their expectation had fallen to 2.88%. By March (green line), the prediction was down to 2.38%. In just six months, the Fed’s outlook for their own interest rate had fallen 24%.

The Fed is getting plenty of heat these days but many people have looked foolish when trying to predict interest rates. Jamie Dimon, head of the largest U.S. bank, recently whiffed.

One takeaway: nobody knows what future interest rates will be. Absent luck, correctly forecasting future interest rates would require accurate prediction of:

- Countless economic data points

- The collective sentiment of millions of market participants

Another takeaway: the headlines surrounding monetary policy greatly overemphasize its relevance to most Americans. Don’t forget that the Fed only controls one rate —the rate at which banks lend each other money overnight. That rate has a loose relationship with other interest rates such as government bonds and mortgages, but it has no discernible effect on arguably the most important rates for average Americans: what they’re paying on credit card debt and receiving on cash in their savings accounts.

Moving a chunk of cash to a higher-yielding savings account or paying down credit card debt is a much better use of your time than losing sleep over Fed policy.

Disclaimer: