The Real World Beckons: Sending Our Children Off with Solid Financial Advice

I am filled with mixed emotions as my oldest son, David, is graduating from college in May. I look back at the advice I gave him four years ago: how to make his savings last four years, how to negotiate living with a roommate, and how to do his own laundry. He has done a pretty good job with the first two, but may have missed the lesson on separating brights from whites.

Happily, David is graduating with a job. He worked hard, interviewed diligently, and will be moving to Chicago to work for a regional bank. After four years at a college near home, he will now be five hours away and truly on his own.

As parents, my husband and I want David to be financially independent with an eye on the long term right from the start. And, as a wealth advisor, I would be remiss if I didn’t equip him with the financial tools to succeed.

The first thing I have told him is the same advice my father gave me: live below your means and always pay off your credit cards in full each month. If you can’t afford something today, save until you can.

I have worked with David on a budget and assessing needs versus wants. Arguably, today’s “wired” world has more “must have” expenses than when I started my first job. Cable, smart phones, and wi-fi internet access are nearly as essential to young professionals as a place to live – and can be quite expensive. Given these additional costs, he is working to cut spending in other areas such as housing (sharing an apartment with two friends) and transportation (living close to the subway to avoid car/parking costs).

Controlling spending is the first step — and saving is the second. Unfortunately for David, he is part of the Gen Y/Millennial generation, predicted to be the first in U.S. history to not do as well financially as their parents. With slower economic expansion, financial security for this generation is likely to require more self-discipline — and aggressive saving — from the very start.

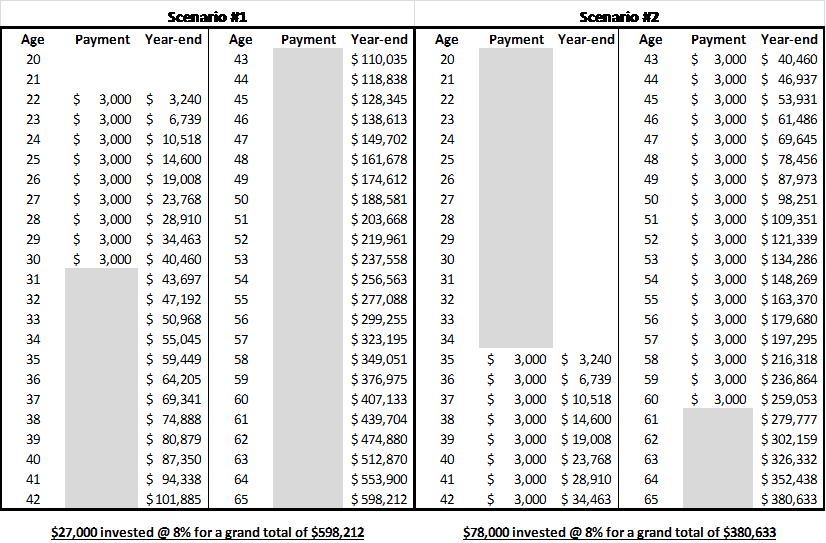

The chart below illustrates the importance of starting to save at an early age. In scenario 1, the student saves $3,000 per year for nine years from ages 22-30 and then nothing more. The student in Scenario 2 waits until age 35 to start, and then saves $3,000 a year for 26 years from ages 35-60. Due to the opportunities for growth provided by the longer timeframe, Student 1 actually ends up with a considerably higher balance at age 60, despite a much lower original investment ($27,000 saved by Student 1 versus $78,000 by Student 2).

I always recommend that clients pay themselves first and take advantage of any employer match on a 401(k) or 403(b) plan. Never pass up free money! Although I generally believe you can never save too much, it is important to strike a balance between the present and the future. I recently had a discussion with a young adult new to the work force who had been saving very aggressively. However, he had so little disposable cash left each month that he felt he couldn’t go out with friends for dinner or buy concert tickets. We ended up adjusting his retirement deferral from 8% to 6%, but with automatic increases of 1% per year to coincide with his annual raises. This allows him to save for his future without entirely sacrificing life in the present.

A Truepoint colleague wrote an excellent piece about helping young adults transition to financial independence. She recommends budgeting using the 50/30/20 rule: spend 50% of your after-tax income on needs, 30% on wants and 20% on savings. This guideline helps maintain a good balance between living for today and saving for tomorrow.

We all hope our children will be self-sufficient as adults, but there may be occasions when we feel we need to help. Although we don’t want to keep our children on the family payroll indefinitely – and certainly don’t want to jeopardize our own retirement needs – my husband and I have decided that if our children ever do need assistance, we would prefer helping them meet the 20% savings goal by contributing to a Roth IRA, rather than helping pay off credit cards.

So, as we send our oldest off into the real world, we hope we have set the groundwork for him to make responsible financial decisions. I will leave him with a new Roth IRA, a clean check register and… a big box of SHOUT® Color Catcher® washer sheets.